Is Our Country Living Beyond Its Means?

-

Wendell Brock

- Oct 10, 2023

- 2 min read

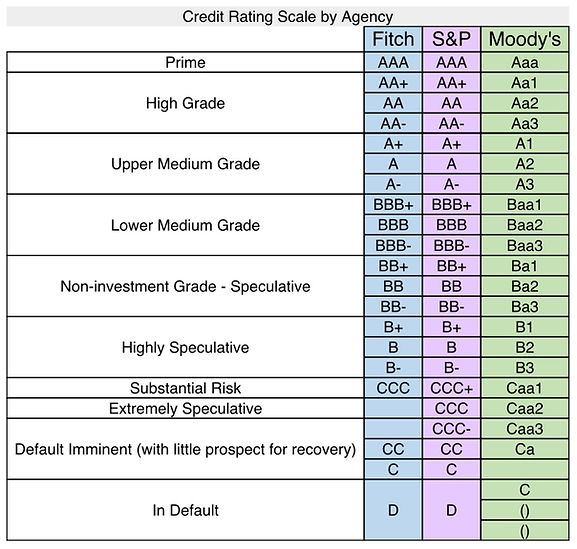

On August first of this year, Fitch Group, one of three top credit rating agencies in the United States, announced a decrease in the credit score of the United States, taking it from a AAA rating to a AA+. This credit rating expresses the forward-looking opinion of the Fitch Group as it looks at the strength of the institution’s ability to pay back its debts. Back in 2011, Standard and Poor’s downgraded the US for the first time in the U. S’s history. Both times have come after issues and debates regarding the debt ceiling.

While neither hit was a huge drop, investors use these rating systems to gauge whether certain investments are likely to default or yield a reliable return, for lending and borrowing decisions, as well as strategic planning. Most economists and investment specialists believe there won’t be too many investors bothered by the decrease, especially those that have a long-term investment strategy.

The immediate concern regarding the downgrade by Fitch was that it could potentially weaken the foundation of trust that our global financial system is built on, calling into question whether the U.S. government will be able to pay back its debts. If the investors that hold the U.S.’s debt lose that trust it could result in something similar to a bank run, in which our government would have to pay back more than what they have available. The downgrade can be seen as a red flag alerting that the U.S. government has a spending problem, which erodes confidence in their fiscal management.

Luckily, in the after-hours trading following the downgrade, the U.S. Treasuries held steady. Politicians and economists immediately assured investors and citizens alike that the downgrade was “arbitrary and of no concern”. However, global news reports expressed unease and questioned the U.S. government’s ability to manage their debt and called into question their governance system. This is a great concern, which our politicians must address, they can’t go forward piling on more and more debt.

Since 2002, the federal government has run a deficit. That means each fiscal year, spending exceeds revenue, which then is added to the national debt. It is projected that spending will continue to outpace revenue by increasing amounts each year, forcing the government to borrow more every year to fund its operations.

In order to receive an upgraded score with Fitch and restore their previous good standing, the government will have to bring down their deficits, which are currently three times the AAA rating median. (Meaning of the 10 countries with a AAA, rating our country is running a deficit 3 times higher than the median of those 10). They will also have to implement long-term fiscal solutions and will have to show that their governance is on the mend.

With our national debt over 44 trillion, the federal government is clearly living beyond its means. Addressing our national debt is critical in securing our national economic future.