Russia: Oil Crisis

-

Wendell Brock

- Apr 20, 2022

- 2 min read

Global geopolitical events have historically affected oil and gasoline prices worldwide as production and supply issues evolve. As the largest oil producer in the world, the Unites States accounts for roughly 20% of total world production. Saudi Arabia accounts for 12% and Russia accounts for 11% of total world production. Even though Russia only produces 11% of total production, it accounts for over 10% of total world oil exports, making it one of the largest exporters of oil and a key global provider.

After their invasion of Ukraine, the imposed sanctions on Russia affects these markets since essential payment methods have been restricted, thus not allowing Russia to fulfill ongoing transactions. The result is a butterfly effect, affecting the rest of the world. The International Energy Agency noted that global oil markets were already tight before the Russian invasion, and commercial inventories have been at their lowest levels since 2014, thus compounding global supply constraints.

According to Eurostat, European countries import about 30% of their petroleum products and about 40% of its natural gas from Russia. The major gas/oil pipelines make their way across Ukraine from Russia to European countries in the western part of Europe. Ukraine has been charging Russia billions to use these pipelines since Ukraine broke free of Russia in the early 1990’s. It’s not just Europe that is feeling the ramifications of current events, we’re experiencing it here in the United States as well.

Even though the U.S. has curbed much of its appetite for oil and gasoline over the past few years, demand among emerging economies has increased. Fossil fuels, including natural gas, petroleum, crude oil, and gasoline still account for roughly 80% of energy consumption worldwide according to the International

Energy Agency. Since oil is a primary energy source, rising oil prices can quickly translate into higher prices in different parts of the economy.

Inflation, as measured by the Consumer Price Index (CPI), is made up of various components, including energy, food, and transportation. These three components represent about 20% of the CPI, all of which are directly affected by oil prices. As a larger portion of consumers’ budgets is spent on these three, the less disposable funds consumers will have to spend on other items.

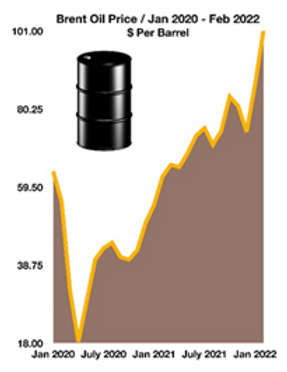

Crude oil is priced in two primary markets, international Brent and as domestic West Texas Intermediate (WTI). Both are priced per barrel and determined by multiple factors, including production, supply, demand, economic growth, weather, and geo-political issues. Unfortunately, Brent and WTI prices had already been rising due to supply constraint issues and increasing demand. The emergence of the Ukrainian conflict has propelled prices even higher, eclipsing $100 per barrel for Brent in February, a level not reached since 2014.