The Inverted Yield Curve

-

Wendell Brock

- Mar 6, 2023

- 1 min read

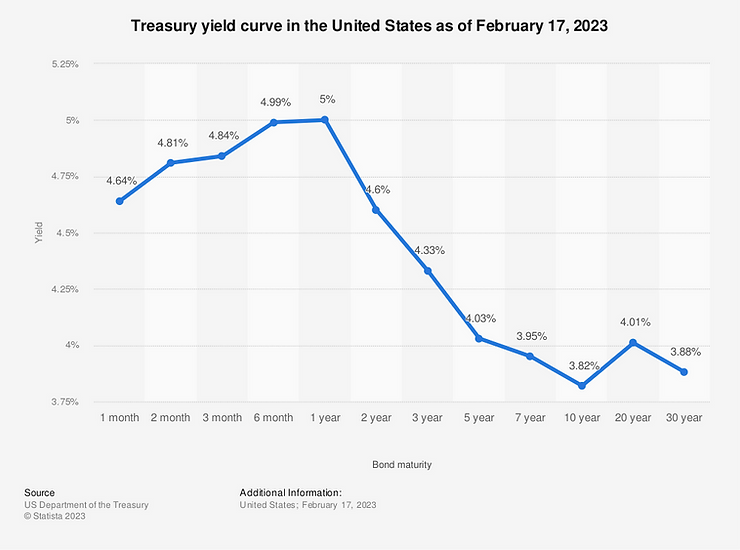

Increasing worry from investors about the financial future can lead to what is called an “inverted yield curve.” An inverted yield curve is where investors pay more for short term bonds than long term, which indicates they do not have a great deal of confidence in long-term financial conditions. Historically, the last five U.S. recessions followed an inverted yield curve.

40-year highs in inflation and Federal Reserve rate hikes played havoc on bonds throughout 2022, sending short and long terms rates to levels not seen in years. Short-term rates remained higher than long-term rates at the end of 2022, indicating a continued inverted yield curve.

The 10-year Treasury note yield started 2022 at 1.52%, peaked at 4.25% on October 24th, and closed the year at 3.88%. The three-month Treasury bill rate, thanks to the Fed’s continuous increase of short-term interest rates to alleviate inflationary pressures, started the year at 0.06% and closed the year at 4.42%.

As of February 2023, the yield for a ten-year U.S. government bond was 3.82%, while the yield for a two-year bond was 4.6%. This again shows that bonds of longer maturities bear a lower yield, reflecting investor’s expectations for a decline in long-term interest rates. This will make long-term debt holders more open to risks under the uncertainty concerning the condition of financial market in the future.

Sources: Federal Reserve, U.S. Department of the Treasury and Statista Research Department.